Dedicated public sector employees often accumulate a substantial amount of vacation time, sick leave, and other retirement incentives over the course of their careers. This accumulation adds up to what may seem like a sizable cash payout once the employee makes the leap into retirement; however, it can also amount to a significant tax liability for that individual—and for their employer as well. While cash payouts are often standard protocol for retiring public sector employees, these perceived “cash windfalls” may not set them up for the secure retirement they had envisioned and earned.

Factors That Are Overlooked

Payroll compensation is subject to FICA and Medicare withholding up to 7.65% for both employee and employer, which means large cash payouts at the time of retirement have tax ramifications for both parties. Additionally, the employee will pay federal income tax on the gross payout. For the sake of example, let’s assume an employee is entitled to a lump sum of $40,000 at retirement and they’re in a tax bracket of 22%.* The employer will be on the hook for $3,060 in FICA and Medicare taxes. The employee will be subject to the same $3,060 in FICA and Medicare taxes, plus federal income tax of $8,800. The $40,000 lump sum has just been reduced to $28,140. That can be quite a blow to a retiree’s sense of security.

Heading into retirement, a well-prepared public sector employee will have done all the math— that is, they’ve calculated their assets and savings (such as pension benefits, accumulated leave payout, and projected Social Security earnings) and compared them to their spending plan. However, during employment, the major share of their health insurance cost was likely paid by their employer. As a result, they can easily overlook planning for this expense in retirement and may not be prepared for what their health insurance will cost without the benefit of employer-subsidized coverage. On average, single retirees pay a monthly premium of $650.** Those who haven’t reached the Medicare eligibility age of 65 will be facing significant out-of-pocket health insurance costs. For them, bridging the gap between retirement and Medicare is imperative.

Two Powerful Solutions

Fortunately, there are tax-advantaged alternative benefit plans that can reduce, and even eliminate, the blow of a hefty tax bill. There are two options widely used among public sector agencies that are each powerful alone, but even better when paired together—the Special Pay Plan and the Health Reimbursement Arrangement (HRA).

Special Pay Plan

With a Special Pay Plan, accumulated leave and other retirement incentive payouts are tax-deferred, eliminating the 7.65% FICA and Medicare taxes for both employer and employee. The funds have the potential for investment growth—tax-deferred—and do not incur federal, state, or local income taxes until they are withdrawn. Once withdrawn, the funds can be used for any purpose. Further, a retiree may be in a lower tax bracket by the time they withdraw their funds, which would mean a lower tax liability than the hypothetical 22% referenced earlier.

Health Reimbursement Arrangement (HRA)

Like the Special Pay Plan, the HRA also allows accumulated leave to be paid out in a tax-advantaged manner. HRA funds are used to pay for qualified medical expenses, as determined by the Internal Revenue Service (IRS). With the HRA, the employee receives a triple tax benefit:

- Funds are deposited into the HRA by the employer free of FICA and Medicare taxes (up to 7.65%).

- Earnings on invested HRA funds are untaxed.

- Reimbursement of eligible medical expenses, including health insurance premiums if applicable, are completely tax-free.

As an added benefit, the HRA can be used by the participant, their spouse, and any eligible dependents. The HRA is a tax-efficient vehicle that maximizes the retiree’s ability to pay for health care, thereby bridging the gap between retirement and Medicare eligibility.

A Winning Combination

While the Special Pay Plan and the HRA are valuable benefit options in and of themselves, the value is augmented when the two work in concert. A benefit program can be designed to divert accumulated leave payouts into two different buckets—Special Pay and HRA—and the allocation percentage can be determined by the employer and/or bargaining group. The result is a “best of both worlds” scenario with tax-deferred funds that can be used for anything and tax-free funds to pay for health care.

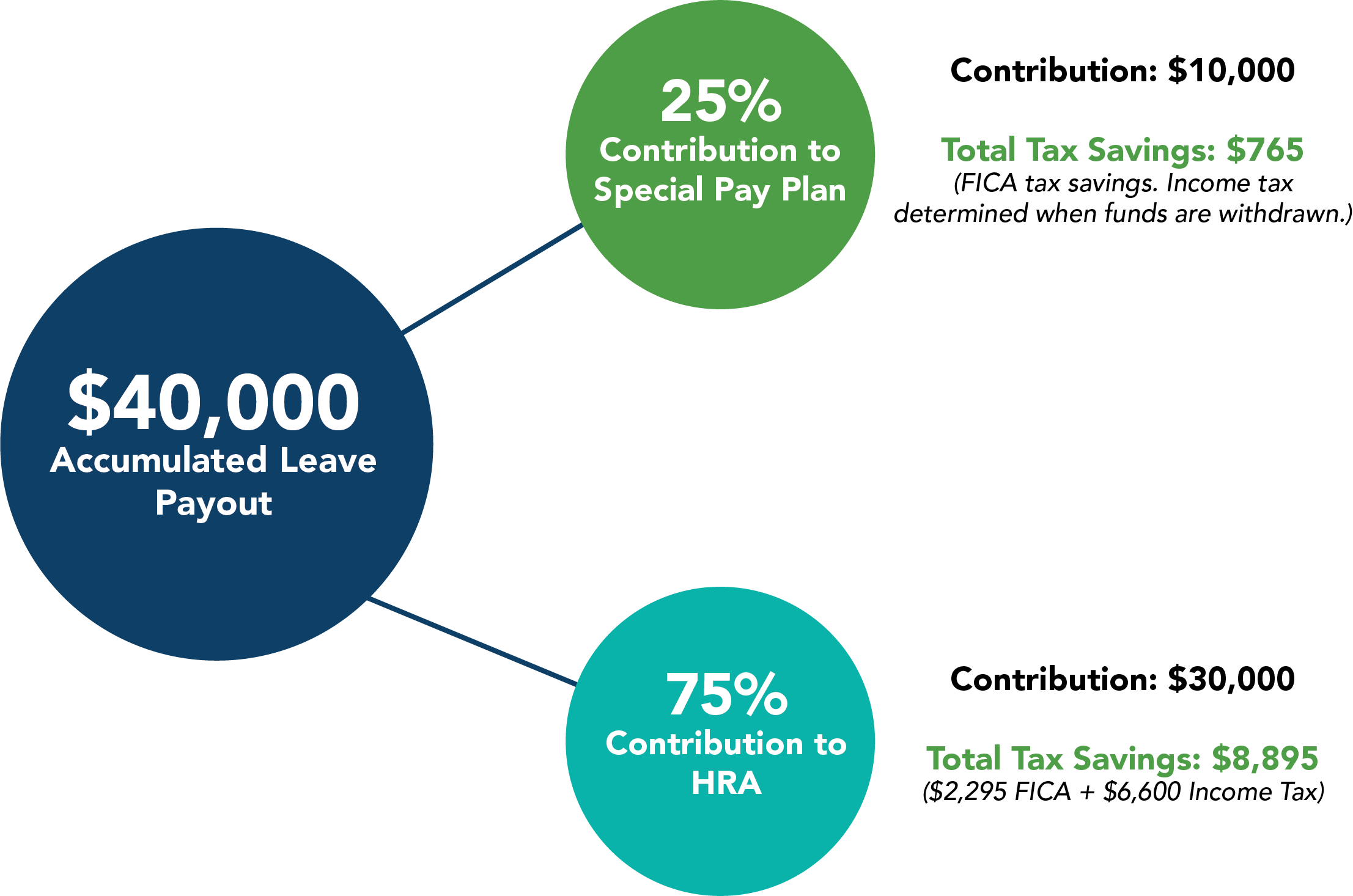

To demonstrate just how a Special Pay/HRA combination would benefit a retiree, let’s use the $40,000 lump sum payout in another example. If 25% of that $40,000 were diverted to a Special Pay Plan, the retiree would have $10,000 available for use upon age eligibility with taxes deferred until the time of withdrawal. If the other 75% of the $40,000 payout were placed into an HRA, the retiree would have $30,000 to pay for eligible medical expenses with a $0 tax liability.

The diagram above illustrates an immediate tax reduction of $9,660 across both plans. A deposit of $30,000 into an HRA would enable a retiree to pay for 46 months of health insurance, based on an average premium of $650 per month.

The Special Pay Plan and the HRA are simple to understand, easy to implement, and highly impactful in terms of maximizing employer savings, stretching retiree dollars, and leveraging tax-advantaged opportunities to realize a healthy, financially secure retirement.

Download our Accumulated Leave Case Study!

Want to learn even more about alternative ways to pay out accumulated leave once an employee retires? Download our case study!

*Based on an average salary at retirement of $60,000. Consult your tax advisor for the actual tax rate that would apply to you.

**2019 average single retiree premium (MidAmerica survey)