If you’re like most people, preparing for retirement is an exciting time. You may find yourself daydreaming about kicking back, relaxing, and taking it easy for a change. For those who can’t sit still, perhaps it’s time to start pursuing that bucket list you’ve been working on your whole life. No matter how you decide to spend your golden years, taking some steps now to ensure that you are well-prepared for what lies ahead—emotionally and financially—can help you to retire with peace of mind.

For best results, you’ll want to allow 12 months of careful financial planning and research before you collect those goodbye hugs. Below is an outline of the scenarios you should consider as you plan your path to retirement, and a suggested timeframe in which to approach each step.

12 Months Before Retiring

If you haven’t already considered what your finances may look like once you leave your job, now is the time to take a serious look at your investment portfolio, your health care expenses, and any other financial obligations you may have. To plan a realistic retirement budget:

- Make a list of your expenses, both fixed and discretionary. Financial Mentor offers a wide selection of resources, topics, and calculators to help you get a snapshot of your financial situation and where you want to be.

- Determine your anticipated income, identifying how much money will be coming in and from what sources. Try retirement income calculators like the one available at OneAmerica to establish a safe level of spending based on your age and the size of your savings. If the budget numbers don’t work in your favor, you may need to delay retirement by a year or two and continue saving.

- Get familiar with the retirement benefits available to you. If you have a retirement plan with MidAmerica that is funded while you actively work, you can log into your account anytime to review plan details. If the plan is not funded until you retire or separate from service, contact your Human Resources representative for a copy of the Plan Highlights which will explain what benefit is available to you upon retirement.

6 Months Before Retiring

- Research Social Security scenarios to estimate the best time to begin claiming benefits. Holding off until age 70 will mean your Social Security check will be 76% larger than if you had signed on at the minimum eligibility age of 62. If you’re considering taking on a part-time job in retirement, those earnings will impact the amount of Social Security you receive. Postponing part-time work until you reach the full retirement age of 66 will enable you to earn as much as you want, and your benefit won’t be affected. FinancialEngines.com offers a Social Security Income Planner to help you determine your best strategy.

- Do the math on healthcare costs. Analyze your current healthcare needs and project your potential future needs based on your own health history and that of your family. Find out what your employer offers to retirees in the way of medical, life insurance, long-term care, and any other types of insurance coverage. Your employer may provide coverage that is more attractive than anything you could purchase on your own. If your employer offers a Health Reimbursement Arrangement (HRA) through MidAmerica, you’ll have access to money—tax-free—to cover eligible medical expenses during retirement.

3 Months Before Retiring

- Tell your employer. Employers may require a minimum notification time or permit retirement only at specific times of the year, so you’ll need to be aware of these rules.

- Review your investments. If you have a pension plan, understand how it works and what it will pay you. Find out if it pays out in a lump sum or if it’s an annuity and think about rollover options like an IRA. Move investments from volatile stocks into more stable options, such as annuities. You’ll have time to work out any tax implications if you know in advance what your options are. Be sure to note the name of the plan, who the manager is, and how to contact them with questions, since your Human Resource contacts may no longer be an option after you retire.

- Develop a strategy for withdrawals. It’s important to take all sources of income into consideration to ensure that you’re drawing down your assets in the correct order and not creating unnecessary tax liabilities. A financial advisor can help determine how much you should withdraw and from what sources, and then establish a monthly disbursement schedule. A good example is the Special Pay Plan or the Employer-Sponsored Plan, both of which are tax-deferred accounts, meaning you are not taxed until you withdraw the funds. If your tax bracket is lower after retirement, you could potentially save on tax when you withdraw funds from these types of accounts. They allow you to control the timing of your cash distributions as well as the timing of your tax obligations.

- Make plans for your post-career life. Now that business is out of the way, let’s talk about what you’re going to do with your free time! You should have a plan here as well. Perhaps there is a volunteer project you’d like to join, family you want to spend more time with, an exercise routine you want to begin or relaunch, or a dream trip you’ll now have time to take. Find activities that make you feel energized, fulfilled, and appreciative of all those years you worked so hard to get to this point.

Upon Retirement

You’ve been working hard all these years and now it’s time that your hard-earned benefit dollars work for you. If you have a benefit with MidAmerica, here are some quick tips to get you started.

“JUST RETIRED!” CHECKLIST

- Review your Welcome Kit and Plan Highlights. Once you have officially retired from your employer, we’ll send you a welcome kit and a copy of your Plan Highlights filled with information about your benefit plan. You’ll want to keep this welcome kit. Don’t be tempted to toss it out with the slew of junk mail you receive! This handy piece of knowledge will instruct you on how to access your account online, where to find important forms, how to designate a beneficiary, and how to get in touch with MidAmerica.

- Access Your Account Online. If you haven’t done so already, create an online user account so you can log in and check your account balance, review your investments and transaction history, move and rebalance your funds (if applicable to your plan), and download forms.

- Update Your Contact Information. While you’re logged into your account, you can update your mailing address, email address, and telephone number. Why is this important? We don’t want to lose touch with you just because you’re not working any longer! We may have important information to share about your account, and we’d hate for you to miss out on the educational pieces MidAmerica develops to keep our participants in-the-know about the benefits they have.

For even more help transitioning into retirement, download the full “Just Retired” Checklist by clicking here!

Retirement should be an exciting milestone for you. Fortunately, you have MidAmerica on your side to ensure that this next chapter of your life is fulfilling and maximizes the retirement and health care benefits you have been working towards and can now enjoy. Keep your “Just Retired!” checklist handy at all times

The most common Health Reimbursement Arrangement questions we field are related to claim documentation requirements. Like many retirement and health care benefits, the HRA is regulated through the Internal Revenue Service (IRS). This means that, as your third-party administrator, MidAmerica must adhere to these IRS standards to make sure your plan stays protected and compliant. When you become claims-eligible and begin submitting reimbursement requests, we may follow up and ask for further documentation to verify and approve your claim. The majority of benefits debit card purchases are automatically approved without additional documentation; however, in some rare cases, we may ask for documentation to complete debit card transactions as well.

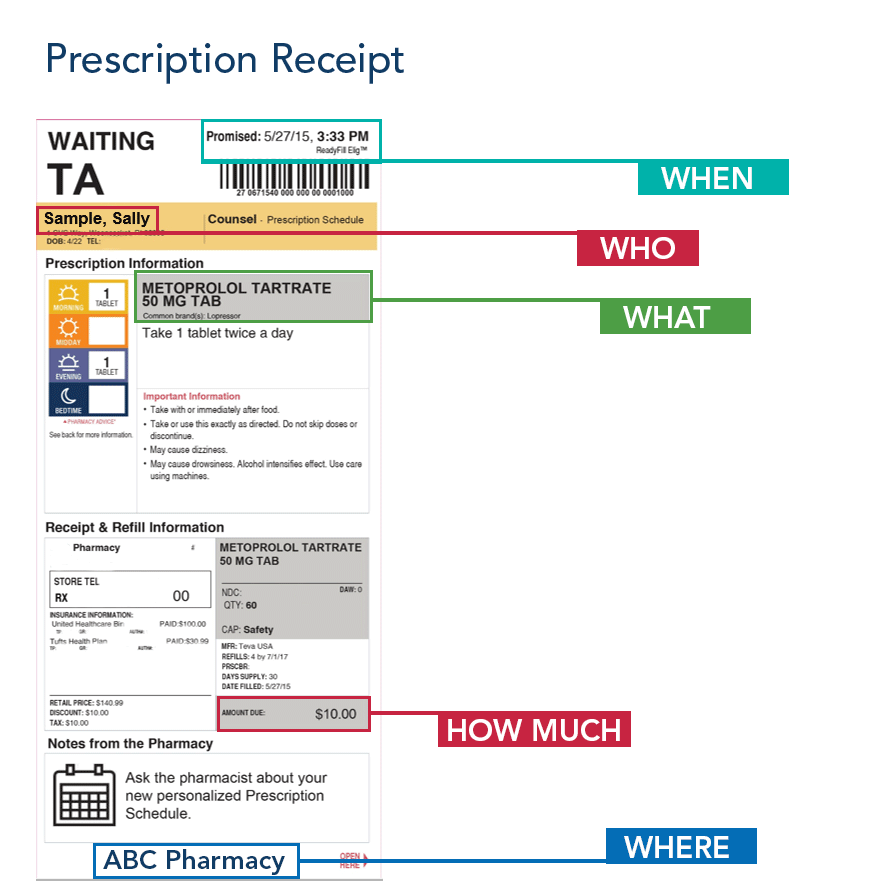

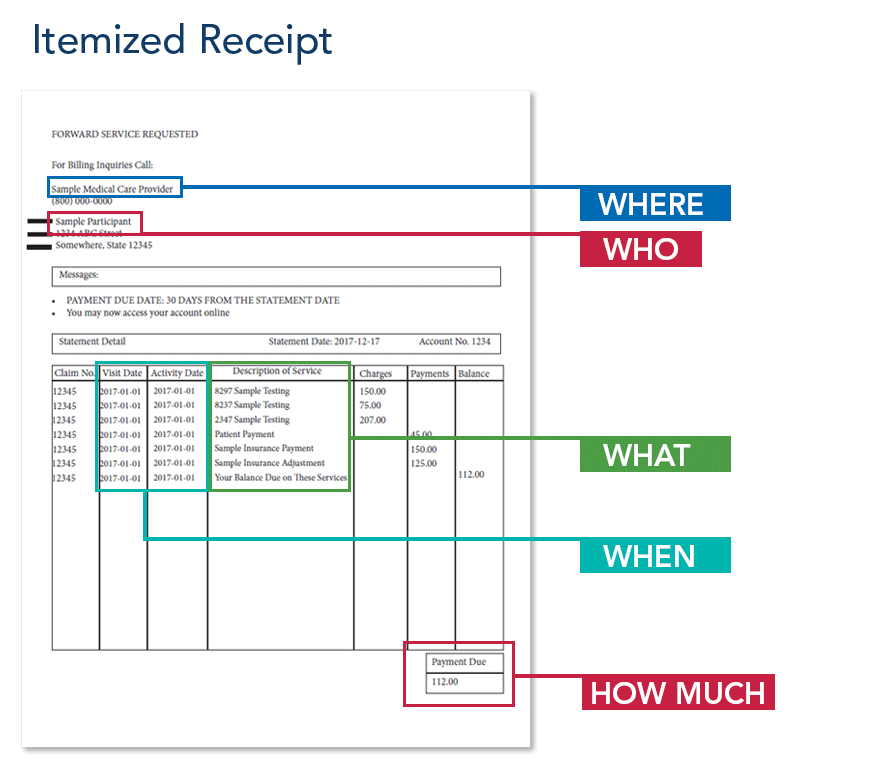

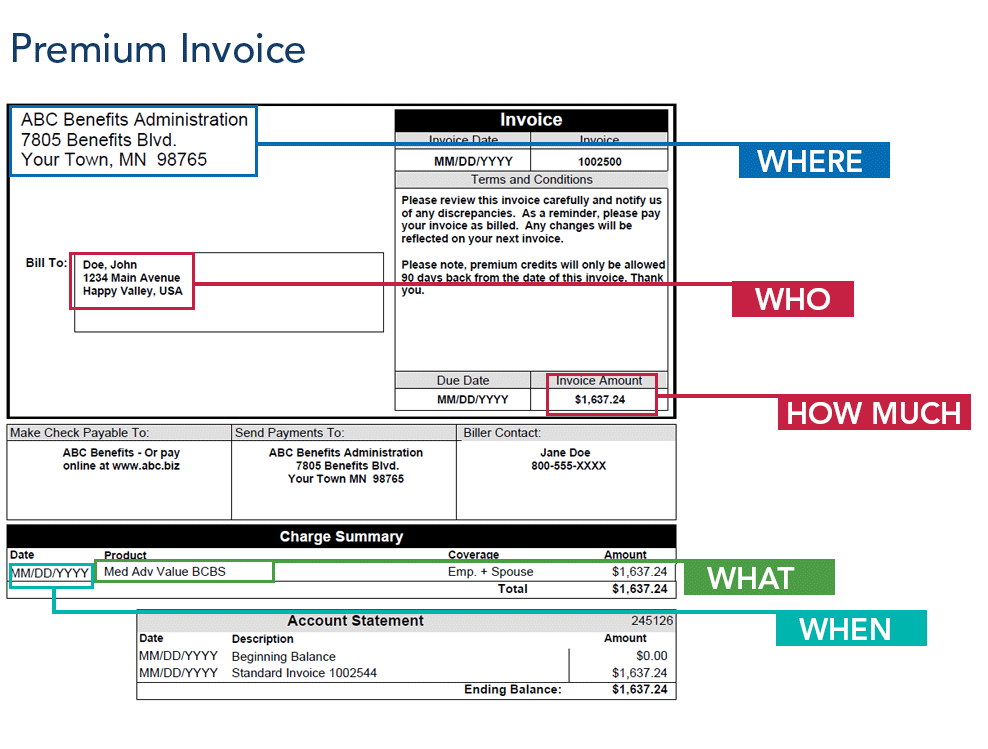

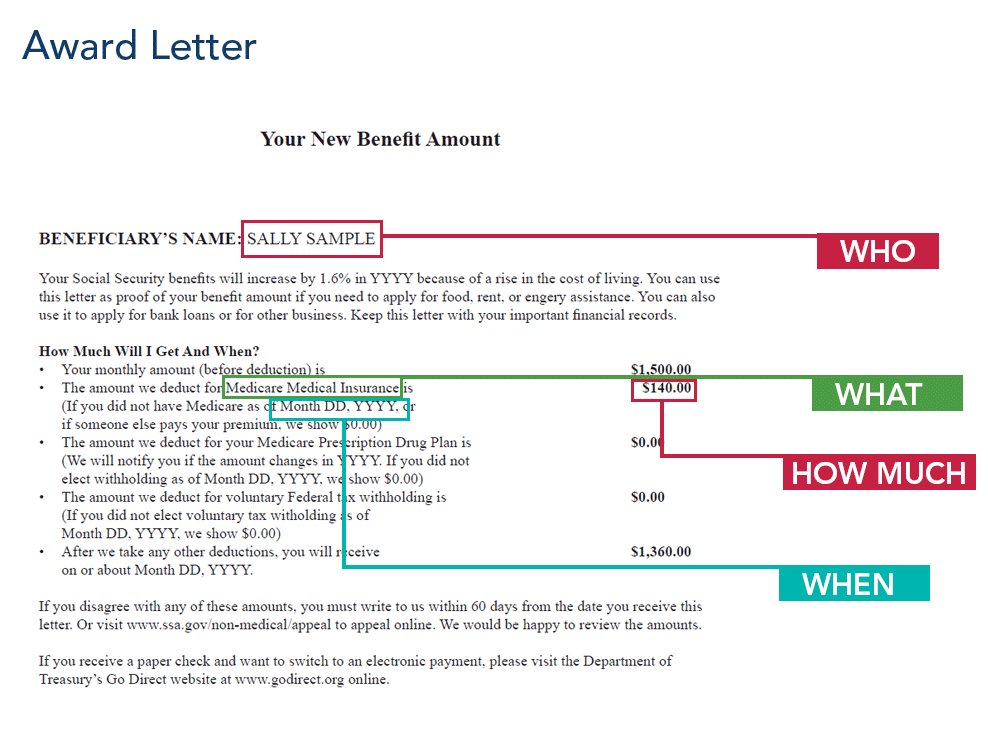

The who, what, when, where and how much of documentation.

Before you submit your claim for reimbursement, take a look at your corresponding documentation and verify that it includes these five elements. Below is a closer look at each key detail:

- Who: This is the name of the patient or, in the case of insurance premiums, the name of the insured person. This could be you, your spouse or an eligible dependent. Ultimately, to protect your benefit funds, we need to see who the medical expense is for.

- What: What is the medical expense? Is it an annual check-up, a prescription refill, or an insurance premium? Your documentation should include a description of exactly what type of medical expense you’re submitting for reimbursement.

- When – There should be some sort of date on the documentation you provide. This could be the date of medical service, the date your prescription was filled, or the coverage period for your insurance.

- Where – Where did you receive medical treatment? Where was your prescription refilled? The name of the provider or pharmacy should appear somewhere within your documentation. For premiums, make sure the name of the insurance carrier is also included.

- How much – How much did the medical expense cost? Your documentation should always include the cost of the service, item or premium you’re submitting for reimbursement.

Examples of Common Documentation

Having an HRA is an excellent way to cover the cost of eligible medical expenses—tax-free—for both you and your eligible dependents. Understanding what IRS-approved documentation looks like can make all the difference in your reimbursement experience and will help ensure a quicker processing time. If you have questions or need additional information, please call us at (855) 329-0095 or email us at healthaccountservices@myMidAmerica.com. We’re always here to help.

Important note on eligible expenses, reimbursement eligibility and debit card access: Eligible expenses, access to reimbursement funds and debit card accessibility under your HRA can vary depending on plan design. For more information on your unique HRA, review the Plan Highlights included with the Welcome Kit you received upon entering the plan.

On March 11, President Biden signed a COVID-19 stimulus bill into law—known as ARPA, or the American Rescue Plan Act of 2021. ARPA increases the amount employees can exclude from their 2021 gross taxable income for employer-provided dependent care assistance program (DCAP) benefits (such as MidAmerica’s Dependent Care Account) under Internal Revenue Code Section 129.

Before ARPA was enacted, the amount that could be excluded from taxation for DCAP benefits through a Code Section 125 cafeteria plan was capped at $5,000, or $2,500 for married individuals filing separately. With the new law, the 2021 limit has been increased to $10,500 (or $5,250 for married individuals filing separately).

This change is helpful for those employees whose DCAPs were amended as a result of the Consolidated Appropriations Act, 2021 (CAA) to allow an additional grace period or carryover of unused funds from 2020 in 2021. With ARPA, those unused funds may be used in 2021 without the participant having to pay additional taxes on amounts over the usual $5,000 calendar year limit.

Because the maximum allowable non-taxable DCAP limit has increased for 2021, it is also possible to amend the DCAP limit to allow elections to the DCAP to be increased to the new limit for 2021.

MidAmerica’s Stance on ARPA

After thorough review of ARPA, MidAmerica will not amend plans to allow elections up to the increased 2021 DCA maximum limit. Here are four notable reasons that influence this stance:

The mid-year election changes may be challenging to allow and could impact tax filings.

If an employer allows their employees to increase their DCA elections for 2021, employees must be cognizant of any unused 2020 DCA funds that are available for use in 2021 due to an extended grace period or carryover provision afforded by the CAA and adopted by their employer. Specifically, it’s wise not to increase the 2021 DCA election to an amount that will exceed the $10,500 exclusion limit that ARPA allows, once any unused 2020 funds are factored in. Any amount of DCAP benefits that exceeds the applicable limit that can be excluded from gross income must be reported to the Internal Revenue Service (IRS) as taxable income. This can be especially difficult to monitor for DCAPs that do not have a calendar year plan year, as the ARPA limit applies to the 2021 calendar year, not the 2021 plan year.

Nondiscrimination rules could be complicated by the DCA limit increase.

It’s important to note that Code Section 129 nondiscrimination requirements have not changed for 2021. These requirements stipulate that DCAPs cannot discriminate in favor of highly compensated employees (HCEs). If a DCAP is deemed discriminatory, any HCEs participating in the DCAP will lose their exclusion from income under Code Section 129, meaning the amount of DCAP benefits the HCE receives for the year will be included in their gross taxable income for that year.

Allowing employees to increase their 2021 DCA elections mid-year up to the new $10,500 limit may create a discriminatory status for the DCA, causing all participating HCEs to lose their income exclusion under Code Section 129.

Unforeseen impacts to 2022 taxable income.

ARPA provides for a higher exclusion limit in 2021 but what happens in 2022? If there is no further legislation to address income exclusion, then any unused DCA funds from 2021 that are available to be used in 2022 will be subject to the previous $5,000 limit, meaning that any eligible expenses over $5,000 that are incurred and reimbursed in 2022 would be regarded as taxable income in 2022. This is especially an issue for plans that operate on an off-calendar year plan year, so that elections made in 2021 will extend into the 2022 calendar year when the deduction limit is lowered.

The introduction of unplanned employer withholding and FICA obligations.

Code Section 129 provides that amounts contributed to a DCA, up to the prevailing allowable limit, are not subject to federal income tax withholding or FICA taxes. However, if an employer were to allow an employee who has a large DCA amount from 2020 that is available for use in 2021, to increase their 2021 contribution election to the new $10,500 limit, it is possible that there could be unplanned withholding and FICA obligations if the IRS did not deem these elections as reasonably excludable from income.

Overall, with ARPA, employees will not have to pay tax on any excess DCAP funds from 2020 that were carried over or used in a 2021 grace period. However, for the reasons noted above, MidAmerica does not recommend amending plans to allow 2021 participant elections up to the temporary DCAP limit.

Click here to download a PDF version of this bulletin.

Traditionally, public sector employers have generously provided some type of employer-paid health insurance benefit for their early retirees (under age 65) as a way to bridge the gap between early retirement and Medicare eligibility. In a time when health insurance was reasonably affordable, it was common to offer what is known as a “defined benefit” plan, in which an employer promises a specific benefit (such as health insurance) over a specific time period.

The Issue

Unfortunately, with premiums rising and budgets being strained, it may be challenging for schools, cities, and counties to plan effectively for the retiree health benefits awarded to former employees now in retirement, or for the health benefits promised to current employees as they retire. Yearly expenditures to fund these benefits become a tremendous liability, draining budgets, and forcing schools to deflect money away from classroom instruction and municipalities to reduce spending on needed services and infrastructure.

The Solution

Employers are now realizing they need to reconsider the benefits packages they offer in an effort to contain costs and long-term financial obligations, yet still provide an impactful retirement benefit to their employees. A Defined Contribution Retirement Plan may be the solution. Contrary to a defined benefit plan which provides a distinct benefit over time, no matter the cost, the defined contribution plan allocates a specific contribution toward that benefit. The contribution is not tied to rising insurance costs, which makes cash flows more predictable, and results in the reduction, or even elimination, of OPEB (Other Post-Employment Benefits) liability. Below are the most noteworthy characteristics that distinguish a defined benefit plan from a defined contribution plan:

| Defined Benefit |

Defined Contribution |

| Reportable OPEB liability under GASB 74/75 |

Eliminates OPEB liability since benefit is fully funded in real time |

| Higher fiduciary liability |

Reduced administrative burden |

| Higher administrative burden due to ongoing funding level reviews, contribution tracking, and benefit eligibility |

Helps attract and retain talent |

How a Health Reimbursement Arrangement Can Help

One of the most ideal funding options for a defined contribution plan is a Health Reimbursement Arrangement, or HRA. The HRA is designed to reimburse employees for their eligible medical expenses to offset their out-of-pocket costs. The employer regularly deposits funds into individual accounts on behalf of employees while they are employed. These funds, along with any earnings from interest, are free from federal income and FICA taxes, and can be used at any time, upon eligibility. To be eligible to use the funds, the participant must have either separated from service or retired. Participants are 100% vested immediately, meaning that they own the account balance as soon as the account is established.

Migrating an employer’s benefit plan design from a defined benefit to a Defined Contribution HRA (dcHRA) will enable that employer to reduce existing liability and minimize future costs, all while keeping its promise to employees and freeing up resources to better serve students, citizens, and the community.

Trusts

Employers may also consider establishing a Trust—like a Post-Employment Benefit or Section 115 Trust—as a vehicle to pre-fund employee and retirement benefits. A trust enables the employer to set aside funds while the employee is still actively employed in order to minimize, or even eliminate, the liability later on. Funding through a trust reduces what can be a substantial liability on the financial statement. The trust is generally considered a separate legal entity and trust funds are safe from the employer’s creditors.

The Advantages of Defined Contribution

The beauty of a defined contribution plan is the built-in versatility of the plan design. With this design, the employer has the flexibility to modify their contribution structure and vesting schedules as time goes on, allowing them to take a “wait and see” approach. All the while, they are reducing their OPEB liability and increasing plan reliability by establishing a Post-Employment Benefit Trust as a vehicle to pre-fund retiree benefits.

To current and prospective employees, the dcHRA is an attractive incentive. It’s a great retention tool that enables employees to see their account balance as contributions are added and interest accrues tax-free over time, making the retirement benefit more tangible. Best of all, employees have the guarantee of a consistent contribution that will provide a tax-free avenue to pay for medical expenses in retirement.

If you’d like to learn how HRAs and trusts can help you achieve your financial goals, contact us today using the form below!

Now that 2021 is well underway, and the new benefits plan years are likely in full swing as well, Human Resources professionals may already be thinking ahead to what next year’s outlook may be. Health care costs continue to rise every year which creates stress for employers and employees alike, as they continuously work to stretch budget dollars further.

When it comes to health care expenses, it seems the only way is up. In fact, the cost of health care has been trending upward for the last several decades. In 1960, health care spending in the U.S. was just 5% of our Gross Domestic Product (GDP). It rose to 13% in 2000, 17% in 2010, and 18% in 2018. According to the Centers for Medicare and Medicaid Services (CMS), the U.S. spent $3.6 trillion on health care in 2018, and costs are projected to reach $6.2 trillion, or 19.7% of GDP, by the year 2028.¹ It’s important to note that these forecasted figures do not take into consideration the COVID-19 pandemic, an ongoing health crisis with a financial impact that is not yet fully known. So, what can be done to meet the challenge of rising medical expenses? Rest assured, there are options available to employers that are looking for ways to contain costs for themselves and for their employees.

Consumer-driven health plans, or CDHP

When we speak of consumer-driven health plans, typically we are talking about Health Reimbursement Arrangements (HRA), Health Savings Accounts (HSA), and even Flexible Spending Accounts (FSA). These plans allow employees to access funds to cover higher cost-sharing provisions in exchange for lower monthly premiums. With employees being more engaged in the cost of health care services, they become better consumers. They may be more inclined to consider the necessity of higher-cost health care in certain situations, e.g. going to an urgent care facility rather than the hospital emergency room. Further, this greater insight into how health care dollars are spent may also persuade them to make positive behavior changes in their lifestyles, such as quitting smoking or exercising more regularly—possibly leading to significant reductions in health plan spending year over year. This is a win/win for both employer and employee. Below is a high-level comparison of the three types of consumer-driven plans.

|

Health Care FSA |

HRA |

HSA |

| What is it? |

An account to help employees pay for eligible medical expenses tax-free. |

An account to help employees pay for eligible medical expenses tax-free. |

A personal bank account to help employees save and pay for qualified medical expenses tax-free. |

| How do you get it? |

Enrollment is through the employer. There is no need to enroll in a health plan. |

The HRA is usually connected to a health plan. If offered, enrollment is automatic when signing up for the health plan. |

Requires enrollment in a high-deductible health plan that meets a deductible amount set by the Internal Revenue Service (IRS). |

| Who contributes to it? |

The employee. The employer can also contribute if they choose to. |

The employer. Employee contributions are not permitted. |

The employee, their family, the employer, and anyone else that chooses to. |

| Can I keep the money if I leave my job? |

No. The employer keeps the money. |

This depends upon plan setup. If the plan has a forfeiture clause, the funds will go back to the employer if the participant leaves. If there is no forfeiture requirement, the participant can retire or separate from service and keep using their HRA funds until they are gone. |

Yes. The employee owns the account. |

| Do I have to pay taxes on the money? |

No |

No |

No |

| What can I pay for with it? |

Medical expenses that are determined by the IRS and the employer. This includes dental, vision, and many other health care services and supplies as listed under Section 213(d) of the Internal Revenue Code. |

Medical expenses that are determined by the IRS and the employer. The employer may only allow the HRA to pay for services covered by your health plan. Some HRAs can be used to pay for dental, vision, and other services/supplies listed under Section 213(d) of the Internal Revenue Code. |

Qualified medical expenses, including services covered by a health plan as well as expenses listed under Section 213(d) of the Internal Revenue Code. |

There are many similarities between the three types of plans, but there are also some distinct differences, particularly in expense eligibility, participation eligibility, design flexibility, and what becomes of unused funds. While HRAs permit reimbursement for health insurance premiums, HSAs and FSAs generally do not. FSAs and HRAs are open to all participants and retirees but HSAs must meet certain IRS-defined eligibility requirements—in addition to enrollment in a high-deductible health plan. And finally, unused FSA funds, and unused funds in HRAs that have a forfeiture clause, will revert to the employer, but HSA funds are completely portable, meaning the employer cannot benefit from unused funds if an employee leaves the company. For more information on CDHP similarities and differences, please click here.

While health insurance premiums will continue to rise, employers have options to potentially reduce escalating costs while still providing a valuable benefit to their employees and encouraging employees to become more invested in their own health care. If you’d like to learn how FSAs and HRAs can help you achieve your financial goals, contact us today using the form below!

¹https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsHistorical

Posted on February 4, 2021

Late last year, Congress passed another COVID-19 relief bill, known as the Consolidated Appropriations Act, 2021 (CAA), which was signed into law by former President Trump on December 27, 2020. This new piece of legislation was enacted to, among other things, extend several provisions of the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

Below please find further explanation of which MidAmerica benefit plans are affected by the CAA and what the new legislation means for participants in these programs.

MidAmerica’s Retirement Plan Amendment Response

MidAmerica has thoroughly reviewed the CAA and, in the best interest of both the participant and the organization, have determined the following retirement plan amendment defaults. If you currently provide a Special Pay Plan, Employer Sponsored Plan, 3121 FICA Alternative Plan or APPLE Plan and do not want the below defaults enabled for your plan, the employer must contact MidAmerica by February 26, 2021.

MidAmerica will default to the following retirement plan CAA amendments:

- Disaster Withdrawals, Hardships and Loans. We will amend the plan to allow these additional provisions in accordance with the CAA.

A Complete Breakdown of the New Rules for Retirement Plans

(Special Pay Plans, Employer Sponsored Plans, 3121 FICA Alternative Plans and APPLE Plans)

The CAA takes disaster relief into consideration and allows additional distributions from retirement plans for those who have experienced economic loss due to a “qualified disaster” (not COVID-related) and whose principal residence is located in a presidentially declared disaster area. A qualified disaster event must have taken place on or after December 28, 2019 and before December 27, 2020 (the date the CAA was signed into law). The event must have been declared a disaster between January 1, 2020 and February 25, 2021.

Under the CAA, plans can be amended to provide additional distribution opportunities for individuals to receive withdrawals or loans if they were affected by such a declared disaster.

Disaster Withdrawals.

Participants can receive a distribution of up to $100,000 (or their vested account balance, if less) for disasters that began on or after December 28, 2019 and that ended on or before December 27, 2020. The distribution must be taken within 180 days of December 27, 2020 (that is, before June 25, 2021). If the participant is impacted by multiple disasters, this dollar limit applies separately to each disaster.

It’s important to note that disaster distributions are subject to a 10% early distribution penalty and are taxed equally over three (3) years unless the participant chooses to be taxed in the distribution year. The distributions may also be repaid within three (3) years of the distribution date.

Hardships.

Participants may repay hardship distributions or first-time homebuyer distributions taken to purchase or construct a principal residence if:

- they received the distribution 180 days before the disaster or up to 30 days after the disaster period,

- the principal residence was in the disaster area, AND

- the participant did not use the distribution because of the disaster.

If taking advantage of this hardship relief, the participant must recontribute the hardship withdrawal during the period that begins on or after the first day of the incident period of a qualified disaster and before June 25, 2021.

Loans.

The CAA also provides a contingency for participants whose principal place of residence at any time during the incident period is located in the qualified disaster area, and that participant has experienced an economic loss as a result of the qualified disaster. Such “qualified individuals” may be able to take loans for up to $100,000 or their vested account balance, whichever is less. The increased loan limit is available to eligible participants from December 27, 2020 until June 25, 2021.

Additionally, under the new law, there is some relief for new and existing loans, permitting a delayed repayment for plan loans that are outstanding on or after the first day of the incident period of the disaster by one year (or if later, June 25, 2021), provided the payment is otherwise due within the period beginning on the first day of the disaster and ending June 25, 2021.

Amendments for Retirement Plans

The changes outlined in the CAA are not mandatory. However, if the plan sponsor of a governmental retirement plan wishes to incorporate any of the changes, the deadline to amend their plan is the last day of the first plan year beginning on or after January 1, 2024 (or December 31, 2024 for calendar year plans).

With COVID-19 cases continuing to surge in the U.S. and a new administration preparing to enter the White House, the Consolidated Appropriations Act, 2021 will probably not be the last piece of legislation to come out of Washington, D.C. related to the pandemic and its effect on the American economy. MidAmerica will continue to monitor the situation and will provide information as it becomes available.

Have questions? We’re here to help.

If you have questions about the CAA, its impact to your plan or the MidAmerica amendment defaults, don’t hesitate to contact our Account Management team at accountmanagement@myMidAmerica.com. You can also download MidAmerica’s complete CAA bulletin by clicking here.

Posted on February 2, 2021

Late last year, Congress passed another COVID-19 relief bill, known as the Consolidated Appropriations Act, 2021 (CAA), which was signed into law by former President Trump on December 27, 2020. This new piece of legislation was enacted to, among other things, extend several provisions of the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

Below please find further explanation of which MidAmerica benefit plans are affected by the CAA and what the new legislation means for participants in these programs.

MidAmerica’s Flexible Spending Account (FSA) Plan Amendment Response

MidAmerica has thoroughly reviewed the CAA and, in the best interest of both the participant and the organization, have determined the following FSA and Dependent Care Account (DCA) plan amendment defaults. If you currently provide an FSA or DCA and do not want the below defaults enabled for your plan, the employer must contact MidAmerica by February 26, 2021.

MidAmerica will default to the following FSA/DCA CAA amendments:

- The Carryover Rule. If the FSA currently has a carryover in place, we will extend the carryover in accordance with the CAA. If the FSA currently does not have a carryover OR a grace period, we will add the carryover in accordance with the CAA.

- Grace Period. If the FSA currently has a grace period in place, we will extend the grace period in accordance with the CAA.

- Change in Status. MidAmerica will continue to accept election changes at any time for any reason.

- Post-Termination Reimbursements. MidAmerica will not implement this change unless requested by the employer.

- Dependent Care Accounts. MidAmerica will not implement grace periods or carryovers unless requested by the employer.

- Dependent Care Carryforward. MidAmerica will not implement the carryforward unless requested by the employer.

If an employer chooses to implement any of these optional provisions, they must operationally comply with them until they amend their plans to reflect the change(s). Amendments to FSA plans must be completed by the end of the first calendar year after the plan year in which the change is effective. For example, plan amendments for plan year 2020 must be adopted on or before December 31, 2021.

A Complete Breakdown of the New Rules for Medical FSAs and DCAs

The CAA provides employers with greater flexibility to grant their employees access to unused funds after the plan year ends, for both their medical flexible spending accounts (FSAs) and their DCAs, up to and including the 2022 plan year. Both program types will now have more freedom regarding:

The Carryover Rule.

For plans that allow carryover of unused amounts into the new plan year, the previous cap of $550 has been waived. Another distinction is the ability to apply the carryover rule to DCAs. Previously, DCAs could impose a grace period but not the carryover rule.

Grace Period.

Prior to the CAA, the grace period—an extended period of coverage that allows participants extra time to incur expenses by allowing them to use their remaining FSA dollars after the close of the plan year—was permitted for only the first 2 ½ months of the new plan year. With the CAA, the grace period can be extended for a full twelve (12) months.

With the new legislation, the carryover rule and the grace period accomplish the same thing—the full amount of unused dollars at the close of the 2020 plan year can be used in the 2021 plan year. It’s important to note that while both FSAs and DCAs can now apply the carryover rule or the grace period, only one is permitted. The plan cannot have both.

Unused funds in 2022.

Both the carryover rule and the grace period will continue to be applicable to plan years ending in 2021. That means any unused funds can be carried over into 2022, with no cap, OR available for a 12-month grace period in 2022, provided the employer has elected to apply either of these rules to the plan.

Change in Status.

For plan years ending in 2021, employers may now permit employees to change their FSA or DCA elections at any time for any reason. This was previously allowed only if an employee had a change in status event. However, if the plan year does not coincide with the calendar year, participants should be reminded that employee election amounts across plan years cannot exceed the annual contribution limit. The annual contribution limits for FSA and DCA have not been affected by the CAA.

Post-Termination Reimbursements.

Under the new law, if a plan is amended to allow it, employees who cease to participate in a health care FSA during 2020 or 2021 will be able to use their remaining balances through the end of the year in which participation ceased (plus any grace period) without having to opt for COBRA. Previously, employees who stopped participating in a health care FSA could only access their FSA remaining balances if the plan allowed for a run-off period or once they enrolled in COBRA.

For DCAs, employees who cease to participate may be allowed to continue filing dependent care claims for expenses incurred through the end of the year, if their plan is set up that way. This continues to be the practice under the CAA.

Dependent Care Carryforward.

Participants enrolled in a DCA who have a child that turned age 13 in the 2020 plan year may now be reimbursed for expenses incurred after the child’s 13th birthday for the remainder of the plan year. If there is an unused balance at plan year-end, they may be reimbursed in the following year until the child turns 14. Previously, dependent care expenses incurred after the child turned 13 were ineligible for reimbursement.

Health Savings Account (HSA) Coordination

It’s important to note that the CAA has not changed how FSAs interact with Health Savings Account (HSA) eligibility. Employees who participated in a medical FSA for 2020 but who will be enrolling in a high deductible health plan with an HSA for the 2021 plan year will still be subject to the existing limitations imposed on their access to their prior medical FSA funds. To be clear, employees may not contribute to a Health Savings Account (HSA) while participating in a general-purpose medical FSA. Internal Revenue Service (IRS) Publication 969 explains the HSA/FSA interaction rules. Employers will need to consider how the new FSA rules, if implemented, will affect an employee’s eligibility for an HSA in 2021 or 2022.

Amendments for FSAs and DCAs

- The new rules outlined above are not mandatory. Employers may opt to apply some, all, or none of the new rules.

- Employers can choose to which plans they apply the rules. An employer may opt to apply a rule to both medical FSAs and DCAs, to medical FSAs but not DCAs, or to DCAs but not medical FSAs.

- Employers can choose to which plan year to apply the rules. An employer can decide to apply the rules to the 2020 plan year but not the 2021 plan year, vice versa, or to both years.

With COVID-19 cases continuing to surge in the U.S. and a new administration now in the White House, the Consolidated Appropriations Act, 2021 will probably not be the last piece of legislation to come out of Washington, D.C. related to the pandemic and its effect on the American economy. MidAmerica will continue to monitor the situation and will provide information as it becomes available.

Have questions? We’re here to help.

If you have questions about the CAA, its impact to your plan or the MidAmerica amendment defaults, don’t hesitate to contact our Account Management team at accountmanagement@myMidAmerica.com. You can also download MidAmerica’s complete CAA bulletin by clicking here.